By RLFinTax.com – Finance Made Fun

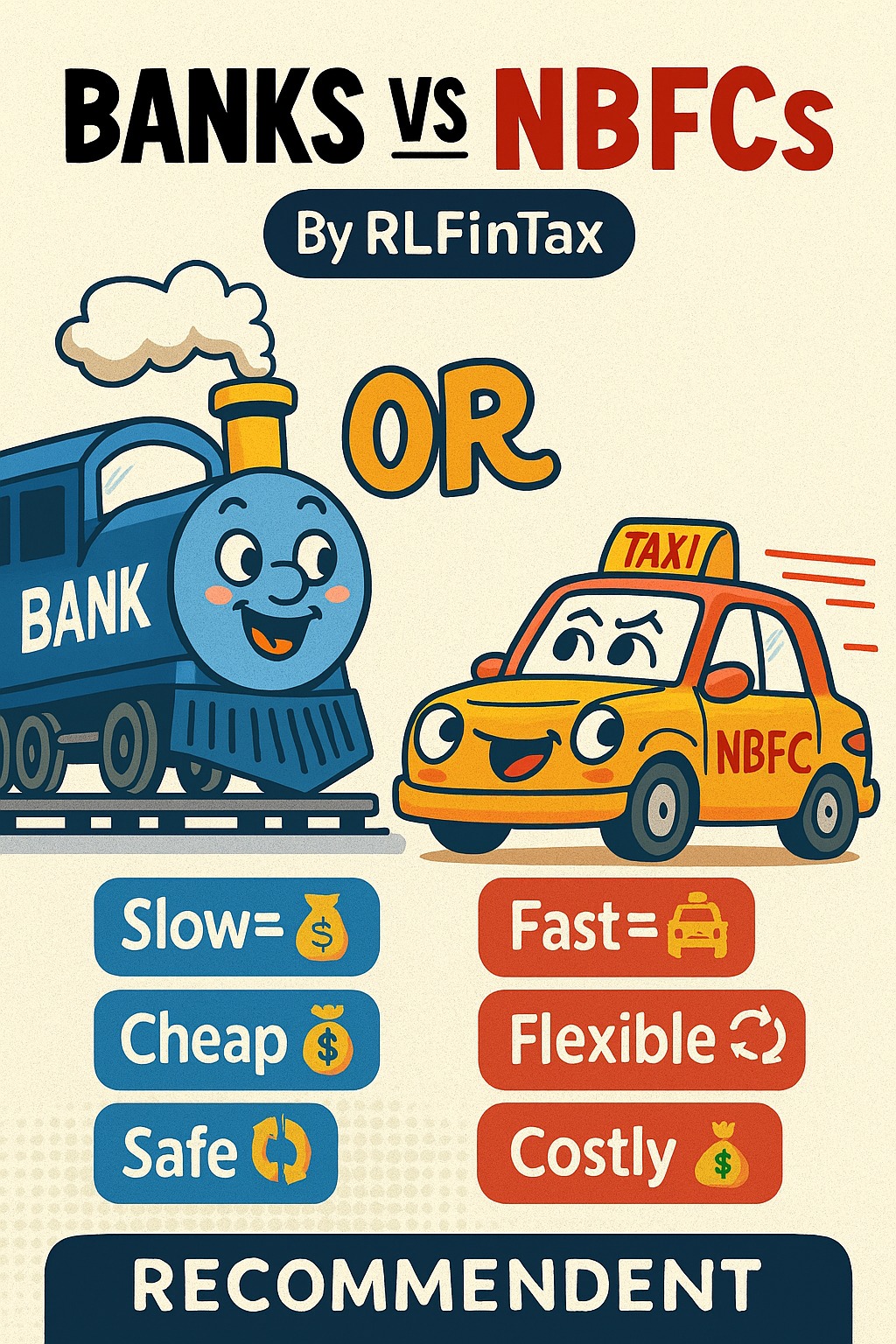

🎭 The Showdown: Banks vs NBFCs

Category | Banks (The Slow but Steady Tortoise) | NBFCs (The Fast but Pricey Hare) |

Interest Rates | Lower, repo-linked. Home loans ~7–9%, business loans ~9–15%. | Higher. Personal loans ~11–24%, business loans ~11–20%. |

Processing Speed | Slow. Think “government office queue.” Weeks of paperwork. | Fast. Think “instant noodles.” Approval in days. |

Eligibility | Strict. Needs strong credit score, audited financials, proof of everything except your blood group. | Flexible. Focuses on cash flow and repayment capacity. |

Collateral | Often required for big loans. | More unsecured options, but at higher cost. |

Trust Factor | Highly regulated by RBI. Safe, stable, predictable. | Less regulated, but still RBI-monitored. Quick and customer-friendly. |

Customer Experience | Formal, reliable, but sloooow. | Friendly, fast, but can pinch your pocket. |

🏦 Why Choose Banks?

- Cheaper EMIs: Your wallet breathes easier.

- Trustworthy: RBI keeps them on a tight leash.

- Big Loans: Perfect for home loans or factory expansion.

- Government Schemes: Subsidies like PMAY, Mudra, and KCC flow through banks first.

🚀 Why Choose NBFCs?

- Speed Demon: Great for emergencies or quick business needs.

- Flexible: Not obsessed with your credit score.

- Less Paperwork: No need to dig out your grandfather’s ration card.

- Tailored Products: SME loans, startup loans, niche funding.

🍜 Example

Need ₹10 lakhs for your business?

- Bank Route: Cheaper (~10%), but approval takes 3–4 weeks.

- NBFC Route: Costlier (~13–15%), but approval in 3–5 days.

👉 If you’re patient, go Bank. If you’re in a hurry, NBFC is your buddy.

📈 RBI Repo Rate – The Puppet Master

- Repo Rate (Nov 2025): 5.25%

- What It Does: It’s like the DJ controlling the loan party. When RBI lowers repo, banks drop their beats (interest rates). When RBI hikes, EMIs dance higher.

- Banks: Directly linked. Your EMI changes with repo.

- NBFCs: Less sensitive. They set rates based on market vibes and risk appetite.

👉 Translation: Banks = cheaper when RBI cuts repo. NBFCs = faster, but less benefit from repo cuts.

🎨 Vibrant Takeaway

- Banks = The tortoise. Slow, steady, reliable, wins in the long run.

- NBFCs = The hare. Fast, flexible, but can cost more.

At RLFinTax.com, we help you pick the right race — whether you need speed, savings, or a balance of both.